Peter Thiel co-founded PayPal, was the first outside investor in Facebook, and runs Founders Fund. Zero to One started as notes from a class he taught at Stanford in 2012, taken by his student Blake Masters and posted online, where they went viral. The book is what those notes became after a serious rewrite. It is short, opinionated, and it does not try to be balanced. Thiel has a thesis and he wants you to agree with it: real progress comes from creating things that did not exist before, not from copying what already works, and the only way to build a great company is to escape competition by becoming a monopoly.

This is a classic for a reason. A lot of the business books published after 2014 are riffing on ideas Thiel already laid down here. If you read just one of them, this is the one.

0 to 1, and 1 to n

Thiel splits all human progress into two kinds.

Horizontal progress is taking something that works and spreading it. He calls this 1 to n. Globalization is the clearest case. China is the example he keeps coming back to: copying 19th-century railroads, 20th-century air conditioning, sometimes copying entire cities from the developed world wholesale. The product already exists somewhere. You take it and replicate it.

Vertical progress is making something that did not exist before. He calls this 0 to 1. The first computer was vertical. The fiftieth laptop is horizontal. Vertical progress is the harder kind, and Thiel argues it is also the kind that actually matters.

The story he could have used but didn’t is the Soviet semiconductor industry. During the Cold War, the USSR decided the fastest way to catch up to American chips was to copy them. They smuggled American chips into the country, often through student exchange programs (a Soviet student named Boris Malin famously brought back a Texas Instruments chip in his luggage in the 1960s), and ordered their own engineers to reproduce them transistor for transistor. The strategy failed. By the time Soviet engineers finished cloning a chip, Moore’s law had already moved the American frontier two generations ahead. The USSR ended up roughly 20 to 30 years behind the United States in computing, and never recovered. They could copy the design. They could not copy the supply chain, the manufacturing process, or the pace of iteration. The result was a permanently second-rate industry that collapsed along with the Soviet Union itself. Pure horizontal progress, with no vertical progress underneath, is a dead end. The USSR is the cleanest historical proof of Thiel’s argument.

His point about the China example is sharper than it sounds. If the whole world adopts American levels of consumption using only the technology we have today, the planet runs out of resources. Globalization without new technology is unsustainable, not just slow. The reason vertical progress matters more than horizontal progress is not that copying is bad. It is that copying alone, without invention, eventually hits a wall.

Reading this in 2026, the China point lands differently than it did in 2014. China is no longer just copying. BYD, DJI, Shein, ByteDance, Huawei in many domains, are doing real 0-to-1 work, sometimes ahead of American counterparts. The horizontal-only China that Thiel describes is mostly the China of fifteen years ago. But the underlying claim, that copying alone runs out of room and you need invention to keep going, is exactly what China figured out. China stopped being a pure copying economy precisely because copying stopped being enough, which is just the USSR lesson learned in time.

The 0-to-1 / 1-to-n distinction is the most useful frame in the book. Not everything has to be 0-to-1 to matter. Iteration is real. But as a way of asking “is what I’m building actually new, or am I just adding another option to an already-saturated market,” it cuts cleanly. When I think about the AI app I’m building, the honest answer is that the model layer is firmly 1-to-n (everyone is wrapping the same APIs), but the interface layer, the way memory and model selection and search disappear into a single chat, has a chance of being 0-to-1. That clarity is useful.

The four dogmas after the crash

To understand why the four dogmas matter, you have to understand what came right before them.

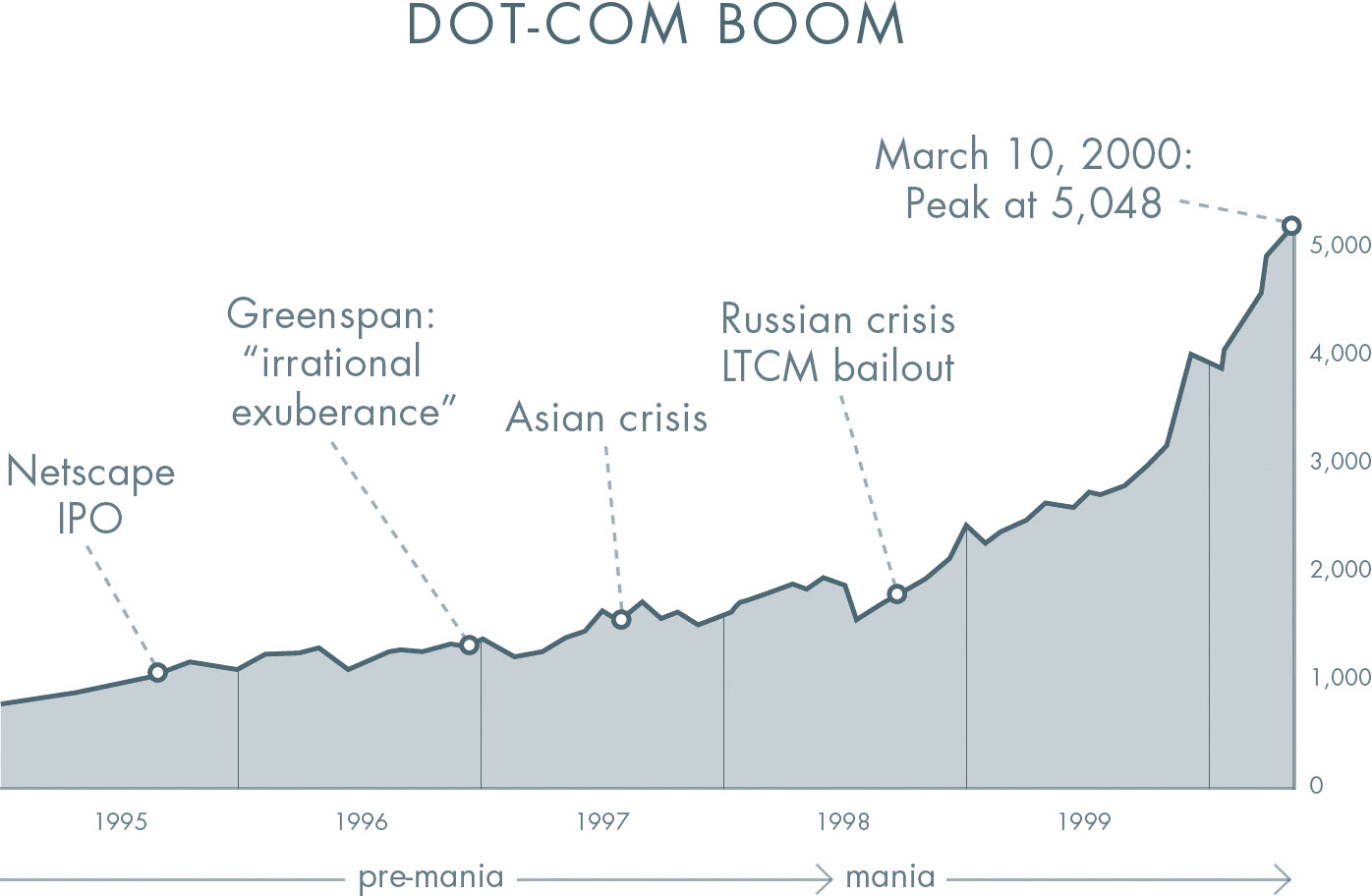

In the late 1990s, the internet looked like the future of everything. Companies with no profits, sometimes with no revenue, were going public at billion-dollar valuations because investors believed the web would eat the entire economy. The metric of success was “page views” and “eyeballs,” not earnings. From September 1998 to March 2000, the NASDAQ basically tripled. People quit jobs to start dot-coms. There were Super Bowl ads from companies that would not exist in eighteen months.

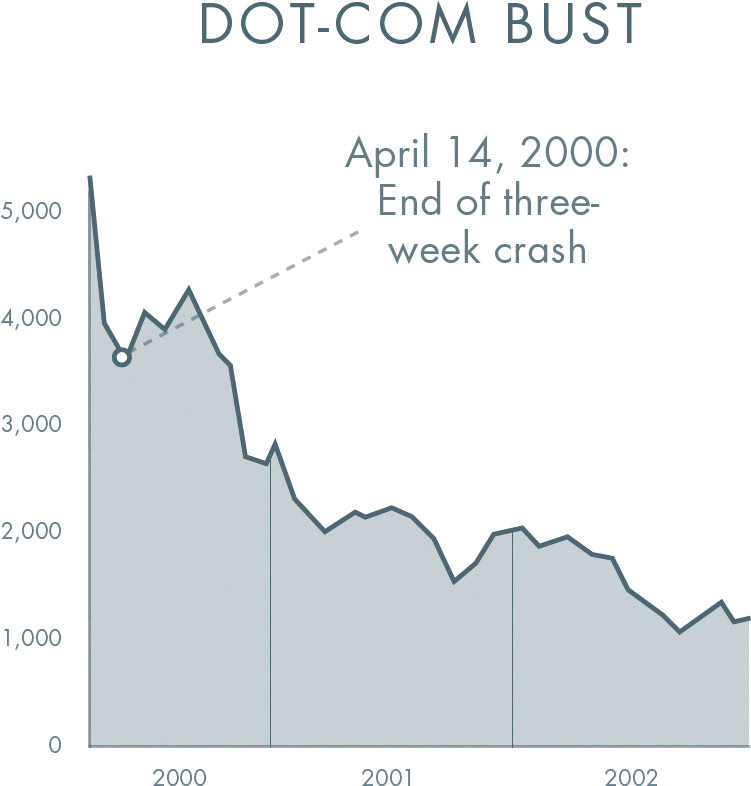

In March 2000, the bubble popped. The NASDAQ peaked at 5,048 and then collapsed. By October 2002 it was at 1,114, down nearly 80 percent. Trillions of dollars in paper wealth disappeared. Hundreds of dot-com companies went bankrupt. Pets.com and Webvan became the punchlines that taught a generation of investors not to trust grand visions.

After the crash, Silicon Valley settled on four “lessons learned” that hardened into doctrine:

- Make incremental advances. Grand visions inflated the bubble, so small steps are the only safe path.

- Stay lean and flexible. Planning is arrogant. Iterate, pivot, treat entrepreneurship as agnostic experimentation.

- Improve on the competition. Don’t try to create a new market. Start with an existing customer and build something better than what they already use.

- Focus on product, not sales. If your product needs salespeople, it isn’t good enough.

Thiel says all four are overreactions. They were the right lessons to learn from the specific failures of 2000, but they got generalized into rules that now block the kind of work that matters. His version of the opposites:

- It is better to risk boldness than triviality.

- A bad plan is better than no plan.

- Competitive markets destroy profits.

- Sales matters as much as product.

The line that ends the chapter is the one I keep going back to: the most contrarian thing of all is not to oppose the crowd, but to think for yourself. Most of what passes for contrarian in tech (going to a hackathon and pitching the same AI agent idea everyone else is pitching, or scrolling on X.com and disagreeing with whatever the loudest voice is saying that week) is just a different flavor of consensus. Real contrarian thinking is harder, because it asks you to actually figure out what you believe before checking what other people believe.

Competition is an ideology

This is the chapter I keep thinking about.

Thiel’s claim is that competition, the thing economics textbooks treat as the engine of progress, is destructive at the company level. Two firms making nearly the same product end up obsessed with each other, copying each other’s features, and grinding their margins to zero. His example is airlines vs. Google. U.S. airlines move millions of people a day and capture about 37 cents per passenger trip in profit. Google moves much less in absolute dollars but keeps 21% of revenue as profit, because nobody else owns search. Airlines look enormous and are barely surviving. Google looks like a single company in one category and is worth more than the entire airline industry combined.

He also makes a sharp point about how companies lie about their markets. Non-monopolists describe their business as the intersection of impossibly narrow categories so they sound unique. Thiel’s example is the restaurant that calls itself “the only British food place in Palo Alto,” as if the relevant market were British food in Palo Alto rather than restaurants in Palo Alto, where it is one of dozens. Monopolists do the opposite. They describe themselves as a tiny player in a massive market so they don’t sound like monopolies. Google describes itself as a small player in the global advertising market, even though it owns roughly 68% of search and search is what its actual business is. The framing is strategic in both cases, and once you see the trick you start noticing it everywhere.

His framing of competition is almost literary. He says rivals are like Shakespearean characters, not Marxist ones. They fight not because they are different, but because they are nearly identical, and they become obsessed with each other for that exact reason.

The stories are good. Microsoft and Google spent years copying each other’s product lines, browser vs. search, OS vs. Chrome OS, mobile vs. mobile. While they were locked into that, Apple ignored both and ate the smartphone market. By 2013, Apple was worth more than Microsoft and Google combined. The two companies obsessed with each other lost to the company that refused to play.

PayPal and X.com is the more personal version. Worth clarifying: this is not the X.com that exists today (the rebrand of Twitter that Elon Musk did in 2023). It was Musk’s original online banking startup from the late 1990s. At the time PayPal and X.com were rival companies. Thiel was running PayPal. Musk was running X.com. The two companies had offices four blocks apart in Palo Alto. They copied each other feature by feature. One engineer at X.com reportedly designed an actual bomb. They eventually merged in early 2000 because both sides were more afraid of each other than of the dot-com crash that was about to hit. The merged company became PayPal. Thiel’s point: the merger was not a defeat for either side. It was the only sane move, and they only made it because they finally realized the rivalry was eating both of them.

The argument extends past business. Thiel uses his own life. He interviewed for a Supreme Court clerkship after law school, did not get it, and felt like a failure. Years later a friend told him that if he had won, he probably would never have founded PayPal. The thing he wanted most would have locked him onto a track that ruled out the work that actually mattered.

This is uncomfortable to sit with, especially when you are still inside an education system. Schools sort everyone into ladders that all lead to the same handful of careers. Everyone competes for the same prizes, doing more or less the same activities, optimizing the same metrics. Thiel’s framing points out that even when you “win” this game, the prize is just permission to enter a slightly more elite version of the same competition. The escape is to do something that does not get scored on the same scale at all.

I do not think competition is purely bad. Some level of pressure produces real work. But the warning that you can spend years winning a race that does not actually take you anywhere is worth taking seriously.

The four traits of a real monopoly

Monopolies are the goal. But not every monopoly is durable. Thiel says the lasting ones tend to combine four characteristics:

Proprietary technology. Something you make that nobody else can easily copy. Thiel’s rule of thumb: it has to be at least 10x better than the closest substitute on some important dimension.

This is the part I want to stop on. Before reading the book, I assumed that being maybe 10 or 20% better than what was out there was enough. The reasoning seemed obvious: my product is better, so customers will switch. The problem is that 10% better does not actually move people. Switching costs (learning a new tool, importing your data, retraining habits, telling your team) usually eat 10% improvements alive. People do not abandon a product they already use for a slightly nicer one. They abandon it for something that feels like a different category.

10x is probably not the literal accurate number. Sometimes 5x is enough. Sometimes you need 50x. But the spirit of the rule is right. Your product has to be so much better that the comparison stops feeling like a comparison. PayPal vs. mailing physical checks for eBay payments was not 10% better. It was a different experience entirely. Google’s PageRank vs. the keyword-stuffed search engines of the late 1990s was not an incremental improvement. It was the difference between getting useful results and not. The iPad vs. the earlier Microsoft and Nokia tablets was not a refresh. It was a different kind of object.

The bar is “you’ve changed what the category is,” not “you’ve made the existing thing slightly better.” Once you see this, a lot of failed products start making sense. They were trying to win on 10% improvements in markets where 10% does not matter.

Network effects. A product that gets more useful as more people use it. Thiel covers this in two pages. Andrew Chen’s whole The Cold Start Problem is basically an expansion of this one trait.

Economies of scale. Especially in software, where the marginal cost of one more user is close to zero. The fixed costs of building the thing get spread over more and more customers as you grow.

Branding. A real monopoly on your own brand. But Thiel is careful here: brand without product substance is makeup on a corpse. He cites Marissa Mayer’s Yahoo, which redesigned the logo, bought Tumblr, hired Katie Couric, and watched the company keep declining because none of it fixed the actual product. No technology company can be built on branding alone.

HP is the version of this story Thiel tells in the Secrets chapter, and it is even sharper. Hewlett-Packard rose to a $135 billion market cap by 2000 through actual invention. Color printers, portable laptops, real engineering breakthroughs. Then the company stopped looking for new things to build. After 1999 the leadership traded R&D for branding exercises, consulting deals, the Compaq merger, and years of boardroom infighting. By 2012 the market cap was around $23 billion. The company was still HP. The brand was still recognized. They had just stopped doing the underlying work that made the brand mean something. The lesson Thiel draws is that a company without ongoing innovation is not stable. It is decaying, even if the financials look fine for a few years. The moment you stop building new things, the clock starts running.

Start with a tiny market

This is the most counterintuitive bit of strategic advice in the book, and the one that connects most cleanly to The Cold Start Problem’s atomic network idea:

Every startup is small at the start. Every monopoly dominates a large share of its market. Therefore, every startup should start with a very small market.

The mistake people make is the opposite. They pitch their startup as “1% of a $100 billion market,” as if winning a thin slice of a huge market were easy. It is not. A huge market means huge incumbents, ruthless price competition, and zero leverage. A tiny market means you can dominate it, and domination produces the cash flow and the credibility you need to expand outward.

The expansion pattern is always the same: dominate one niche, then expand into adjacent ones sequentially. Amazon went books, then CDs, then videos, then software, then everything. PayPal went PalmPilot users, then eBay PowerSellers, then general internet payments. Facebook went Harvard, then Ivy League, then U.S. colleges, then the world. eBay started by dominating Beanie Babies, which sounds absurd until you realize that being absurd is exactly the point. The atomic market should look small enough that competitors do not bother to take it seriously.

Thiel also rejects “disruption” as a goal. Disruption originally meant a specific thing: using new technology to enter at the low end and work your way up to displace incumbents. It has been watered down to mean “anything new and exciting.” But more importantly, framing yourself against incumbents invites the exact competition you should be trying to escape. Napster called itself a disruptor of the music industry and was on the cover of Time before it was in bankruptcy court. PayPal explicitly did not frame itself against Visa. It expanded the payments market into spaces Visa was not in. It survived. Napster did not.

The phrase he uses is “last mover advantage.” Being first matters less than being final. The goal is to make the last great development in a market, the version that everyone after you is just iterating on, and capture monopoly profits for years or decades.

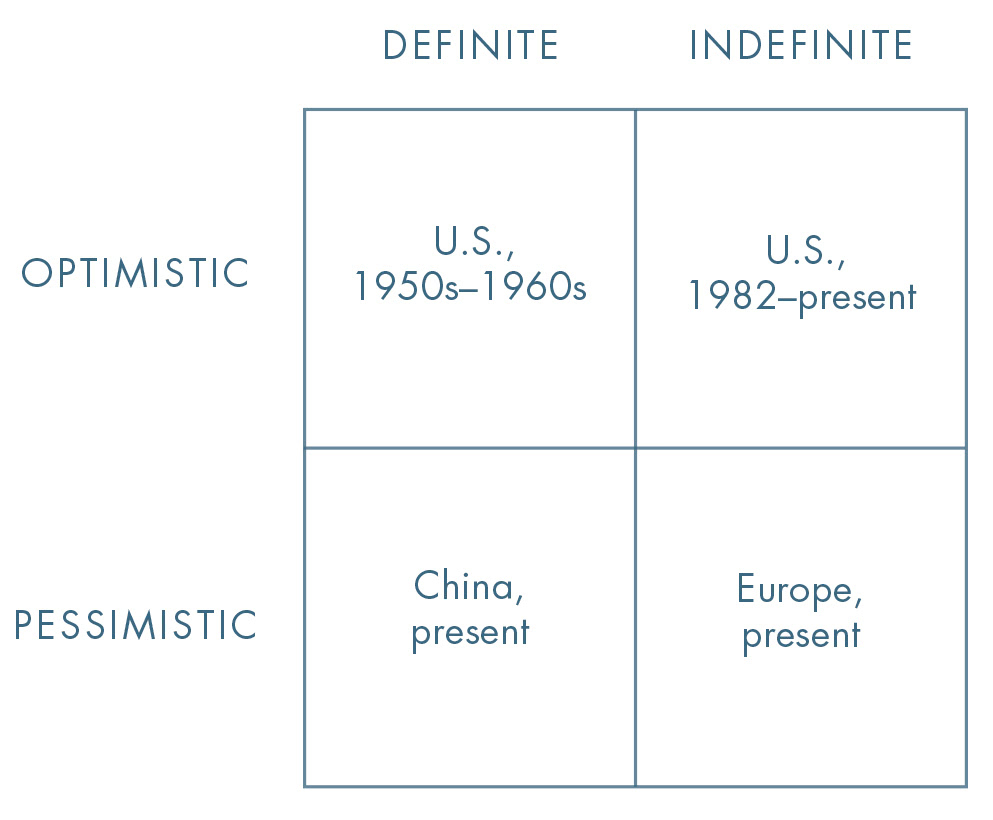

Definite vs. indefinite optimism

This is the chapter I keep coming back to.

Thiel splits worldviews along two axes: optimistic vs. pessimistic, and definite vs. indefinite. That gives four quadrants:

Definite optimism is “the future will be better, and here is the specific plan to build it.” America from roughly the 1950s to 1970s. Apollo Program. Interstate Highway System. Empire State Building. Hoover Dam. Plans were drawn up. People committed. The thing got built.

Indefinite optimism is “the future will be better, but I have no idea how, and we should keep our options open.” Thiel’s diagnosis of America since around 1982. The whole “lean startup” movement, in his reading, is indefinite optimism applied to building companies. Ship MVP, get feedback, iterate, pivot, never commit because committing might be wrong. Finance is indefinite optimism applied to money: rearrange existing assets, hedge everything, preserve optionality forever. The same logic shows up in elite education, where students collect “well-rounded” résumés full of extracurriculars they don’t care about, because nobody can tell them which specific thing to commit to.

Definite pessimism is “the future is going to be worse, and we have a plan to manage it.” Thiel uses China as the example. He frames China’s leadership as quietly believing that the country’s growth will eventually slow, that the global pie will not keep getting bigger forever, and that the rational move is to grab as much of it as possible now. Whether or not that diagnosis is right, the structural point is real: a society can be definite about its future even if its outlook is dark.

Indefinite pessimism is “the future is going to be worse, and we don’t know what to do.” Thiel’s caricature of Europe.

His attack is on indefinite optimism specifically, because it is the one that has captured the West and especially Silicon Valley. The founders he most admires, Jobs at Apple and Zuckerberg at Facebook, were definite optimists. They had multi-year visions. Jobs did not build the iPod by polling users. He had a long arc that went iPod, then iPhone, then iPad, planned out years before users had any way to ask for it. When Yahoo offered Zuckerberg $1 billion for Facebook in 2006, he turned it down because he had a definite picture of what Facebook was supposed to become, and $1 billion was not enough to interrupt it.

I am genuinely conflicted on this one. I have used iteration. AvoidXray is being shaped by what users do, not by some master plan I made on day one. The AI app I’m building is the same way. I’m shipping, watching, adjusting. And that is mostly working.

But I also notice that the projects that go furthest are the ones where I had a clear picture of what I was actually trying to make. Not a fifty-page strategy doc, but a concrete vision. For the AI app, it is “an app where the model selection and the memory and the routing all disappear, and you stop thinking about which AI you’re using.” That is definite. The iteration is around the edges. The center is fixed.

I think Thiel is right that pure indefinite iteration produces small things. But I also think he underrates how much definite vision needs to grow alongside the actual work, not before it. Sometimes you discover what your secret is partly by building. The two are not as opposed as he frames them.

The split between definite and indefinite is the most important framing in the book for me, more than 0-to-1 or monopoly or anything else. It changed how I think about my own plans. Most of what I call “keeping options open” is just refusing to commit, and the refusal is making the options worse, not preserving them.

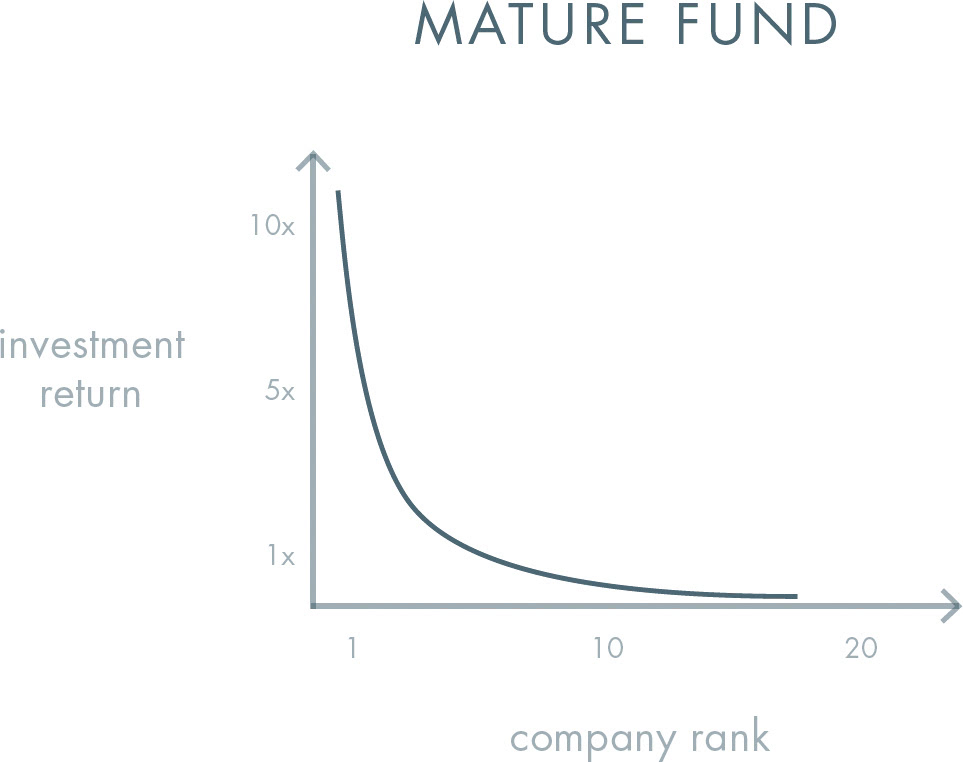

Power laws

Venture capital returns do not follow a normal distribution. They obey a power law. In any successful VC fund, the single best investment usually returns more than the entire rest of the portfolio combined. Founders Fund’s 2005 fund had Facebook return more than every other investment in the fund put together, and Palantir was on track to return more than everything except Facebook. This is not unusual. It is the rule.

The two rules of venture capital that Thiel draws out:

- Only invest in companies that have the potential to return the value of the entire fund.

- Because the first rule is so restrictive, there can be no other rules.

The reason most VCs underperform is that they spread their bets, hedge their portfolios, and end up with a collection of companies that all do okay but none do extraordinarily well. In a power-law world, a portfolio of “okay” is a portfolio of zeros.

Thiel extends this past finance. Power laws govern careers too. You cannot diversify your time across twenty paths the way you would diversify a stock portfolio. Choosing the right company, the right market, the right collaborator, matters exponentially more than accumulating a balanced set of skills. The same logic applies inside a single startup: one market, one distribution channel, a few key decisions, generate almost all the value. Spreading attention evenly across everything is how you guarantee mediocrity.

The line that ends the chapter: you are not a lottery ticket. Outcomes are not random. They are concentrated, and they are the result of specific choices about where to put your time and capital.

Secrets

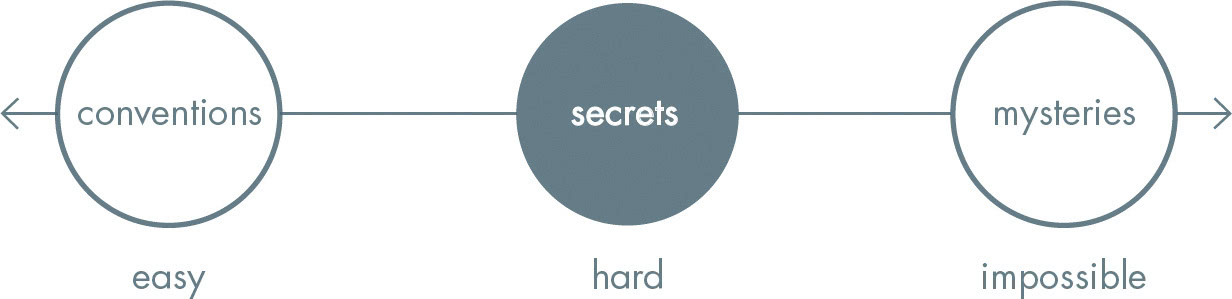

Thiel’s framing of “secrets” is the part of the book that feels most like a worldview rather than a business strategy.

A secret, in his definition, is an important truth that few people know but is achievable. Not a mystery (something nobody can solve), and not conventional knowledge (something everyone already has). It sits in between: hard, but possible.

He divides secrets into two kinds. Secrets of nature are undiscovered facts about the physical world: new physics, new biology, new chemistry. Secrets about people are things people don’t know about themselves, or things they hide because they don’t want others to know.

The interesting claim is that secrets about people are systematically underrated. Airbnb’s secret was that people would let strangers sleep in their houses if the trust system was right. Uber’s secret was that people would get into a stranger’s private car if the app made it feel safe. Both look obvious in retrospect. Both seemed insane when first proposed, and the first reaction from most people who heard the pitch was “no way that works.” The whole point of a secret is that the world is set up to dismiss it. If everyone agreed with you, it wouldn’t be a secret.

Thiel argues we have collectively stopped looking for secrets. Four trends killed it: incrementalism (small steps get rewarded), risk aversion (don’t be wrong alone), complacency (elites collect rents instead of inventing), and “flatness” (assuming a global talent pool of seven billion people has already found everything worth finding). The result is a culture where smart people either pretend ironically there’s nothing left to find, or go full Unabomber and conclude civilization is doomed.

Whether or not you buy the diagnosis, the practical question he forces is useful: what do you believe that almost nobody around you believes? And, just as importantly: is it actually true, or are you being contrarian for its own sake?

I have been turning this over since I finished the book. Most of my “beliefs,” when I tried to write them down, turned out to be repackaged versions of things I had read on X. The exercise of forcing yourself to identify what you genuinely believe and almost no one else does is more uncomfortable than I expected. It is also more useful.

Foundations

This chapter is short and hard to argue with. Early decisions in a company are nearly impossible to undo. Thiel’s law: a company that is messed up at its foundation cannot be fixed.

Co-founder choice is like marriage. Equity splits are like the U.S. Constitution. There have been seventeen amendments since the Bill of Rights, and that’s in over two hundred years. You don’t get to rewrite the rules later.

His specific advice: choose co-founders you have a real prior history with, not people you met at a networking event. Keep the board to three people. Five maximum. Bigger boards are theatre. Everyone full-time, on the bus or off the bus. Pay people in equity, not cash. High cash salaries reward extraction. Equity rewards building.

The PayPal team is the textbook case. Four had built bombs in high school. Five were under twenty-four. Four were foreign-born. Not “diverse” in the modern HR sense, but extraordinarily aligned in worldview and obsession. After the eBay acquisition for $1.5 billion in 2002, that group went on to start SpaceX, Tesla, LinkedIn, YouTube, Yelp, and Palantir. The “PayPal Mafia” is one of the most concentrated outputs of human productivity in tech history, and it came from a tiny, weirdly specific group of people who chose each other carefully.

The principle generalizes past startups. Who you do something with shapes what it becomes. Choose carefully, and choose people who actually share the obsession.

Distribution

Thiel insists this is the chapter most founders skip, and it’s the one that kills them.

The Silicon Valley delusion is that a great product sells itself. He says: it doesn’t. Ever. A product without a distribution plan is a bad business no matter how good the product is. Poor sales rather than bad product is the most common cause of startup failure.

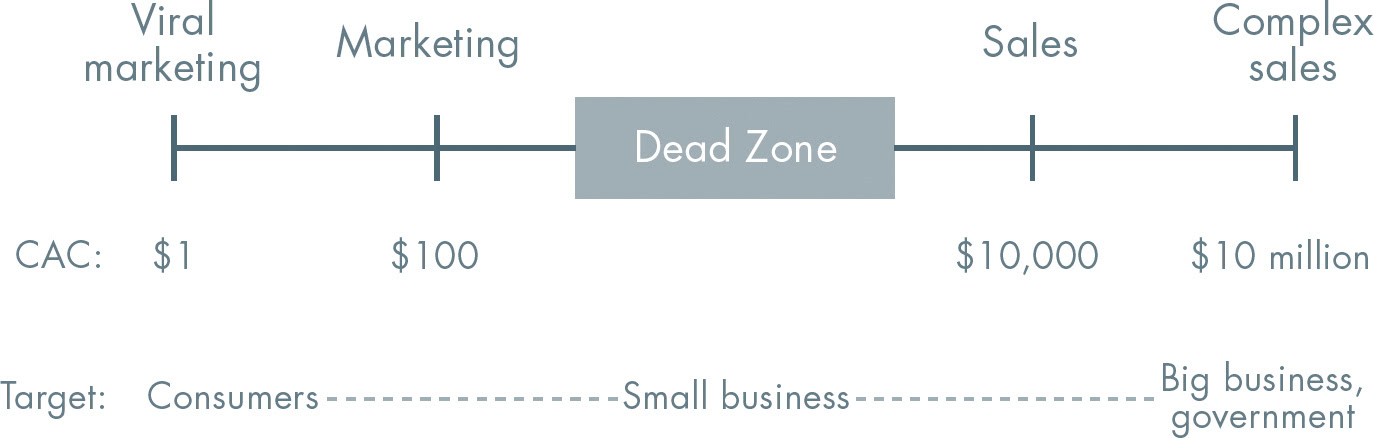

His distribution scale, sorted by deal size:

Complex sales, millions of dollars per deal. The CEO sells personally. SpaceX closes billion-dollar contracts because Elon Musk himself navigates the politics. Palantir’s CEO Alex Karp reportedly spent twenty-five days a month on the road closing deals between $1 million and $100 million each. There is no separate sales force. The CEO is the sales force.

Personal sales, around $100 to thousands of dollars per deal. A sales team builds relationships, one customer at a time. Box, the cloud storage company, started by selling to the Stanford Sleep Clinic, then used that as a reference to sell across the rest of Stanford, then to other universities. ZocDoc had salespeople personally recruit doctors, which doubled as both revenue and improving the network for patients.

Marketing and advertising, mass market. Warby Parker uses TV ads because their roughly $100 price point and customer lifetime value justify the broad reach but cannot support one-on-one selling.

Viral marketing, where the product itself drives invites. PayPal grew by paying $10 to sign up and $10 per referral, then dominated eBay by becoming the de facto payment method for PowerSellers.

A 2026 example I keep thinking about is SlapMac. Someone built a Mac app that screams when you slap your MacBook. That is the entire product. It costs $6.90. The Instagram video of the app working went viral on its own, no ad spend, because the product is its own demo: you slap a laptop, the laptop screams, you film it, people watch, they laugh, they download it. The author reportedly made around $5,000 in the first three days. That is what real viral marketing looks like. The product’s core function is the marketing. There is no separate distribution channel because the channel is the thing itself.

Most of what I’m building falls in that middle band, right around or just inside the Dead Zone. AvoidXray, the AI app, the side projects. Not big enough for Karp-style enterprise sales. Not viral enough that the product sells itself. The Dead Zone is the hardest place to be because there is no shortcut. You actually have to build relationships with users one at a time, get the early ones to bring more, and earn each piece of growth. It is also where most founders fool themselves. They convince themselves their product is going to “grow organically” when it has none of the structural traits that make organic growth possible.

The iron rule across all of these: customer lifetime value must exceed customer acquisition cost. If it costs you $50 to get a user and they generate $30 of value, you do not have a business. You have a slow-motion fire.

He also argues distribution itself follows a power law. Pick one channel and dominate it. The “kitchen sink” approach, where you try TV ads and viral loops and content marketing and outbound sales all at once, almost never works. You need one channel that actually scales, then maybe a second.

The line that landed hardest for me: if you don’t see the salesperson, it’s you. Founders who think they don’t need to sell are the ones spending all their time on Twitter, on demo calls, on investor decks, on conference panels. That is selling. They just don’t admit it.

Computers as complements, not substitutes

This is the chapter where the book is most clearly a product of 2014.

Thiel’s argument: computers are complements to humans, not substitutes. Humans are good at intentionality, judgment, and planning. Computers are good at high-speed data processing. They are categorically different, not just different in degree. The most valuable businesses combine them: software flags patterns, humans render judgment.

His examples. PayPal’s “Igor” fraud system, where automated detection alone failed against adaptive fraudsters, and the working version was a hybrid: algorithms surfaced suspicious transactions, human analysts made the final call. Palantir, applying the same approach to intelligence work. LinkedIn, which gave recruiters tools instead of replacing them, and ended up with 97% of the recruiting industry as users. He uses Google’s 2012 cat-recognition project as the punchline: a supercomputer with 16,000 CPUs scanning 10 million YouTube thumbnails got to 75% accuracy at identifying cats. A four-year-old child does it perfectly. Different in kind, not in degree.

This chapter has aged the most strangely of any in the book. Thiel’s core distinction, that humans and computers are categorically different, was clean in 2014. It is shaky now. AI models can write production-ready code that is genuinely robust, not toy snippets but real software that ships. Algorithms now use AI internally where they used to use hand-tuned heuristics. Most “AI startups” launched in the last two years are essentially wrappers around frontier model APIs, and a real percentage of them are growing fast because the underlying model is doing the heavy lifting that used to require teams of engineers. The line between “things only humans can do” and “things software can do” is moving every six months, and almost always in software’s direction.

That said, the strategic advice still holds even if the categorical claim does not. The most valuable AI products right now are not the ones trying to fully automate humans out of the loop. They are the ones that make humans dramatically more capable. Cursor is not replacing programmers. It is making programmers absurdly more productive. Most of what I’m trying to build follows the same pattern: not a replacement for the user’s thinking, but a tool that makes the user’s thinking more effective.

So I came out of this chapter thinking Thiel got the principle right (build complements) for partly the wrong reasons (computers and humans are categorically different). The principle survives the change in facts. The reasoning behind it is dated.

Tesla and the seven questions

Near the end of the book is the cleantech chapter, which is where Thiel’s framework actually gets tested. In the 2000s, investors poured over $50 billion into thousands of green startups. Most went to zero. Thiel says they failed because almost none of them could answer seven basic business questions:

- Engineering. Can you create a breakthrough, or just an incremental improvement?

- Timing. Is now the right moment for this specific business?

- Monopoly. Are you starting with a big share of a small market?

- People. Do you have the right team?

- Distribution. Can you actually get the product to customers?

- Durability. Will your position hold ten or twenty years out?

- The secret. Have you found a unique opportunity that others have missed?

Most cleantech companies could answer one or two of these and were vague on the rest. They had decent technology but no distribution. They had distribution but no real engineering edge. They had a team but no secret. The market was a graveyard.

Tesla is the example that proves the framework, because it answered all seven correctly.

On engineering, Tesla did not invent a single new battery cell. What they did was integrate existing components into a car that was an order of magnitude better than any electric vehicle anyone had made before. Daimler, Mercedes-Benz, and Toyota all ended up using Tesla’s technology.

On timing, Tesla secured a $465 million Department of Energy loan in 2010, just before government green-energy support became politically toxic. They closed the window before it shut.

On monopoly, they did not try to take on the global auto industry on day one. They started with the Roadster, a $109,000 luxury sports car. They sold around 3,000 of them, and that was the whole point. The market was tiny. It was rich tech millionaires who wanted to look both wealthy and environmentally conscious. Tesla owned that niche completely. From there they expanded to the Model S, then Model X, then Model 3. Same pattern as Amazon going from books to everything. Same pattern as PayPal going from PalmPilot to eBay to the world.

On people, they assembled actual engineers and designers, not subsidy-hunting executives. On distribution, they sold direct, controlling the entire customer experience instead of relying on dealerships. On durability, the brand became inseparable from the founder, and the technology lead compounded. On the secret, Thiel’s reading is the sharpest part. The secret was not that the world needed clean energy. Everyone already believed that. The secret was that wealthy consumers wanted to look cool and green, and that a luxury status symbol was a better wedge into the EV market than an economy car. Tesla built a status symbol first, and an energy solution second.

The seven questions are the most useful framework in the book for anyone actually trying to start something, because they are diagnostic. You can apply them to your own project right now. If you can’t answer most of them, the book is essentially saying: you are about to become one of the cleantech ghosts.

Stagnation or Singularity

The actual closing chapter of the book pulls all the way back from companies and products and asks: what are the possible futures for humanity, and which one are we choosing?

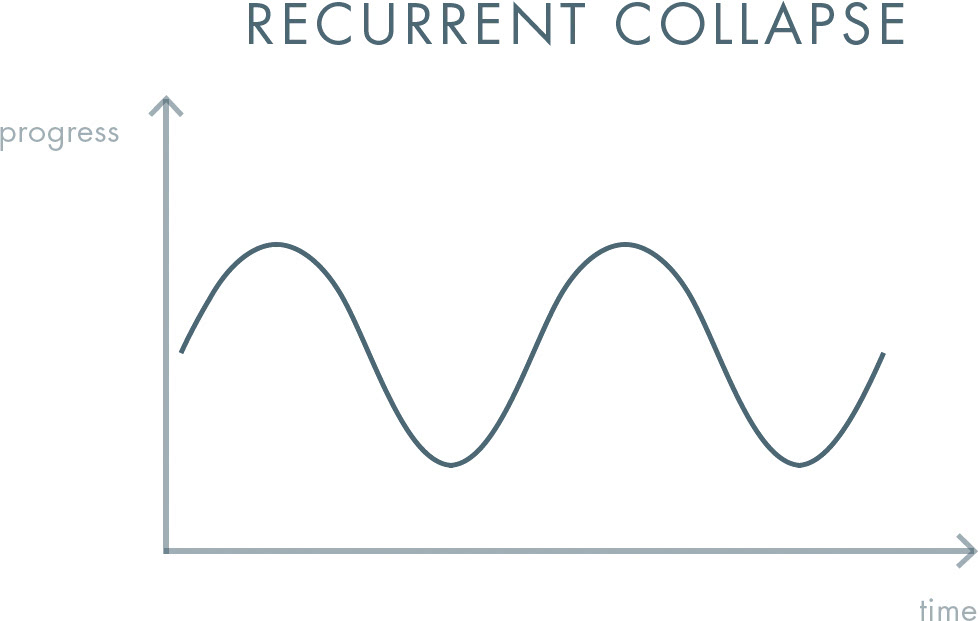

Thiel borrows a framework from the philosopher Nick Bostrom. There are four broad scenarios:

Recurrent collapse. Civilization rises, falls, rises again. Endless cycles of progress and ruin. Thiel argues this one is unlikely now because human knowledge is too distributed to be fully lost. We have too many books, too much infrastructure, too many people who know how things work. A single catastrophe cannot push us all the way back.

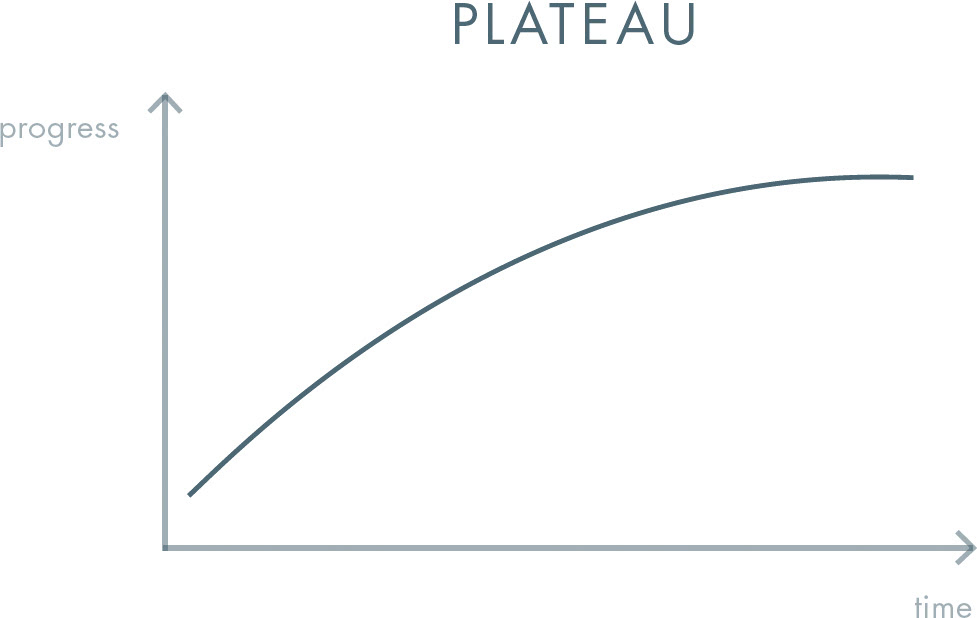

Plateau. Every country slowly converges to the current standard of living of the rich world, and then stops. This is the future most people seem to expect by default. Thiel thinks it is also impossible. Without new technology to ease competition over scarce resources, plateau turns into conflict, and conflict turns plateau into something worse.

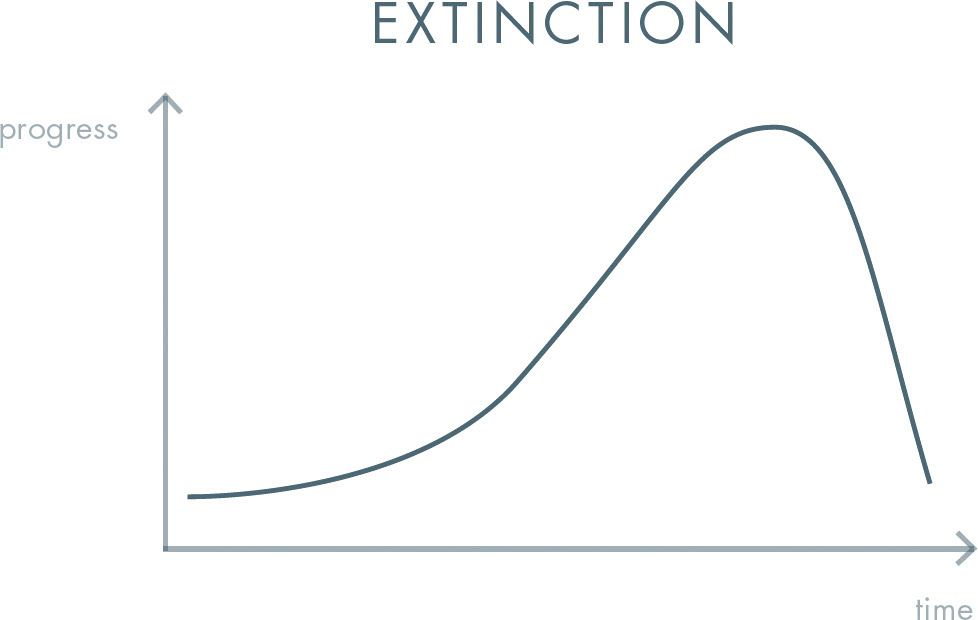

Extinction. The future ends. No more humans. Whether by war, environmental collapse, or some other catastrophe, civilization just terminates. There is nothing more to plan for in this scenario, which is why Thiel spends almost no time on it.

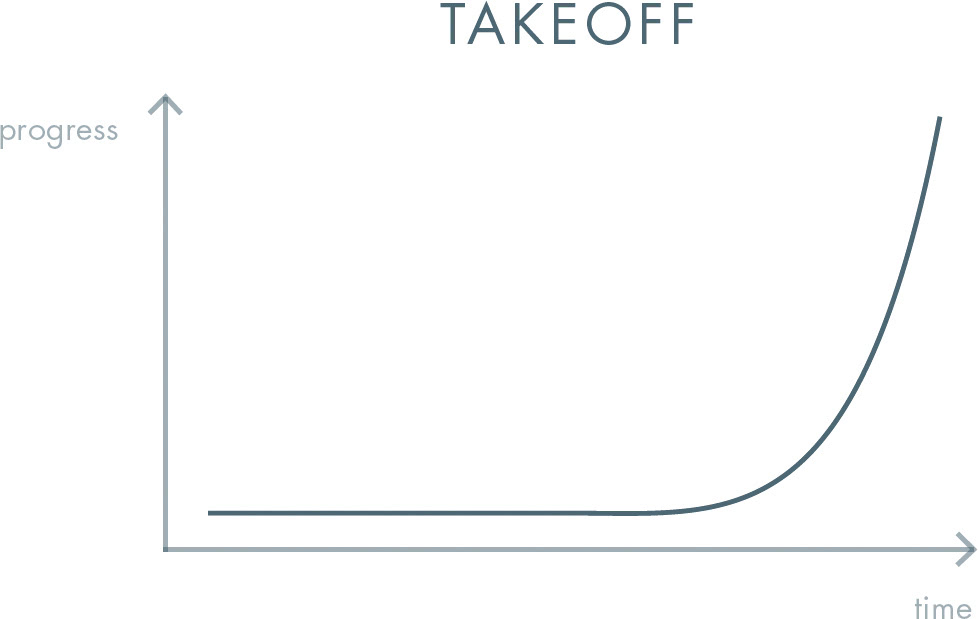

Takeoff. Technology breaks through to a new level. Kurzweil’s Singularity is the most famous version: artificial intelligence that surpasses human intelligence and accelerates everything from there. But Thiel makes clear that he does not need the science fiction version. He just needs the basic idea, that real new technology can change the trajectory.

The argument that ties this back to everything else in the book is the one I find genuinely compelling. Plateau is unstable. Extinction is unplanable. Recurrent collapse is unlikely. The only path that works is takeoff, and takeoff does not happen by accident. Trends do not realize themselves. Singularities are not delivered by some cosmic schedule. They are built, by specific people making specific things, one company and one breakthrough at a time.

The closing line of the book is the one that pulls all 200 pages together: our task today is to find singular ways to create the new things that will make the future not just different, but better, to go from 0 to 1.

That is the entire thesis stated as a personal demand. The 0-to-1 framing at the start of the book seemed like a way to think about startups. By the end, it is a way to think about your own life. What new thing are you actually contributing? If you stripped away your job title and your résumé and your social position, what part of the future would not exist without you?

I do not have a satisfying answer to that question yet. But the question itself is the right one to be sitting with at this stage, and I’d rather be uncomfortable with it now than wake up at 40 having never asked it.

Zero to One vs. The Cold Start Problem

I read these two books back to back, and they overlap and disagree in interesting ways.

Where they agree. Both want you to start with the smallest market or community you can dominate. Thiel calls it monopolizing a niche. Chen calls it the atomic network. Both think network effects are one of the most important sources of long-term defensibility. Both think distribution is underrated and that great products do not sell themselves.

Where they disagree. Chen’s whole methodology is iterative, empirical, bottom-up. Find what works, repeat it, refine the playbook across cities or campuses or user segments. Thiel’s whole methodology is the opposite. Have a definite vision. Commit. Build the future you can already see. If you took Cold Start as your only guide, Thiel would call you an indefinite optimist with a fancier vocabulary. If you took Zero to One as your only guide, Chen would point out that most of the companies Thiel admires actually iterated their way to the vision, even if they tell the story afterward as if it were planned all along.

Cold Start is a tactical book about how networked products specifically grow. Zero to One is a philosophy book about how progress works at all. They are written for different reasons and they answer different questions. The honest take is that you need both. The Thiel framework gives you the questions to ask before you build. The Chen framework gives you the playbook to use once you start. Reading only one of them leaves a real gap.

My take

The strongest parts of Zero to One are the ones where Thiel attacks an idea most people accept without examining it. The four post-2000 dogmas. The myth of healthy competition. The illusion that being a first mover matters more than being a last mover. The cult of indefinite optimism. The chapter on competition alone is worth the price of the book. The Tesla breakdown at the end is the clearest worked example of his framework anywhere in the text.

The weakest parts are the ones where Thiel’s politics or temperament leak through. His diagnosis of “indefinite optimism” sometimes turns into a generalized grumpiness about modernity. The Founder’s Paradox chapter, with its detour through scapegoat kings, ancient Aztec rituals, and the 27 Club, is interesting but pretty far from anything actionable. And the Man and Machine chapter has not aged well, even if its core advice survives.

The book is also a product of one specific person’s success. Thiel co-founded PayPal, made an early bet on Facebook, and has built or backed several companies that genuinely went from 0 to 1. He has earned the right to be confident. But the confidence sometimes shades into “anything that does not look like what worked for me is wrong,” and a lot of valuable companies do not look like PayPal. Stripe iterated. Notion iterated. Linear iterated. Many billion-dollar companies are basically 1-to-n businesses done extremely well. Thiel’s framework would say these are less important than 0-to-1 work, and maybe in some long-term sense he is right. But “less important than the iPhone” is not the same as “not worth building.”

The Cold Start Problem gave me a vocabulary for things I was already experiencing. Zero to One gave me something different: a set of contrarian questions to keep asking. What do I believe that almost nobody around me believes? What competition am I in that I should leave instead of win? What 10x improvement am I actually building? What is my definite plan, not my plausibly-deniable optionality?

I do not think Thiel is right about everything. But the questions he forces are the right questions, and most other business books I have read do not even try to ask them. That is why Zero to One is a classic. Twelve years after publication, the questions still cut.

Concepts I’ll carry forward

- 0 to 1 vs. 1 to n. Am I creating something new, or just spreading something that already works.

- The contrarian question. What important truth do very few people agree with me on.

- Escape competition, don’t enter it. Similar players obsessed with each other miss the actual future.

- The 10x rule. Real monopolies need order-of-magnitude advantages, not feature parity plus polish. 10% better does not move people. The product has to be so much better that the comparison stops feeling like a comparison.

- Start with the smallest market you can dominate. Same lesson as the atomic network, framed as monopoly.

- Last mover beats first mover. The goal is to be the final player in a category, not the earliest.

- Definite over indefinite. Have a real plan, not just preserved optionality.

- Look for secrets, especially about people. The biggest opportunities hide in things people don’t see or don’t admit.

- Foundations are permanent. Who you start with and how you set up equity will determine how everything later goes.

- Distribution is not optional. Every founder is also a salesperson, whether they admit it or not.

- Power laws govern everything. A few decisions, a few people, a few moments produce almost all the value.

- You are not a lottery ticket. Outcomes are concentrated, intentional, and earned, not random.

- The seven questions. Engineering, timing, monopoly, people, distribution, durability, secret. If you can’t answer most of them, your project is in trouble.